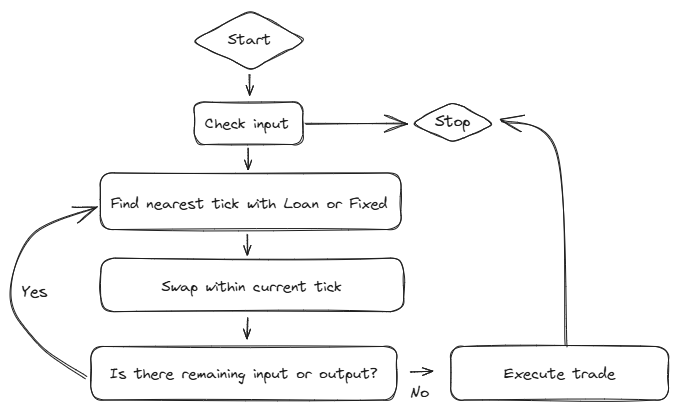

Swap

The swap function is the central mechanism for swapping between Fixed Tokens and Loan Tokens. When swapping, the protocol finds the nearest tick with a positive balance of the output token. Using the tick bitmap, the protocol processes liquidity in the following order per tick:

- Partially filled limit orders.

- Unfilled limit orders.

This ensures that at all times, on a per tick basis only 2 batch ids can contain liquidity. The AMM's swapping mechanism is similar to Uniswap V3 as it loops through ticks.

Parameters

PoolKey key: Contains pool configuration (tokens, maturity, tick parameters).int256 amount: The amount to swap. A positive value indicates exact out, while a negative value indicates exact in.uint8 limitTick: A boundary tick that limits how far the swap can execute, acting as a form of slippage limit. If the limitTick == 0, then it means the swap must be fully executed spot.uint256 slippageLimit: Represent the minimum amountOut or maximum amountIn required. This acts as the slippage limit.uint256 minLimitOrderAmount: Represents the minimum amount unfilled that has to be placed in the limit order tick after the swap execution.bool isLimitOrder: Determines if any remaining input amount once the limitTick is reached should be added as a limit order.bool loanForFixed: Indicates whether the swap direction is Loan Tokens to Fixed Tokens or vice versa.

Users can specify the direction of their swap (e.g., Lend or borrow) using fixedTokenForLoanToken and specify exactIn or exactOut using the sign of the amount.

Swap Output

amountInFilled: The amount of input tokens consumed.amountOutFilled: The amount of output tokens delivered.limitOrderAmount: The portion added as a limit order.batchId: Identifies the batch of limit order involved (if applicable).

Swapping Mechanics

Slippage Limit:

The limitTick parameter acts as an indication to place a limit order with the unfilled amount.

Remaining Input as Limit Order:

If isLimitOrder is true, any remaining input amount when the limitTick is reached is placed as a limit order.

Non-Deterministic Limit Orders:

If swapping with an exact out amount and isLimitOrder == true, and the swap breaches the slippage limit, the transaction reverts.

Limit orders must be specified with an exact input amount since they execute asynchronously and cannot guarantee an exact output amount.

Exchange Rate Calculation

The exchange rate is determined at each tick by the tick's corresponding interest rate using the exchange rate formula:

User swap exchange rate

Swapper pay fees to liquidity providers and limit order users when swapping. The fee corresponds to bpsPerTick. This is such that:

- When swapping Loan Tokens to Fixed Tokens (lending), users receive Fixed Tokens at the tick's rate minus

bpsPerTick. - When swapping Fixed Tokens to Loan Tokens, users receive Loan Tokens at the tick's rate plus

bpsPerTick.

This means that in the absence of Pool Fees, Liquidity Providers and Limit order users receive a rate that is improved by bpsPerTick compared to the tick at which they added liquidity or a limit order.