Pool

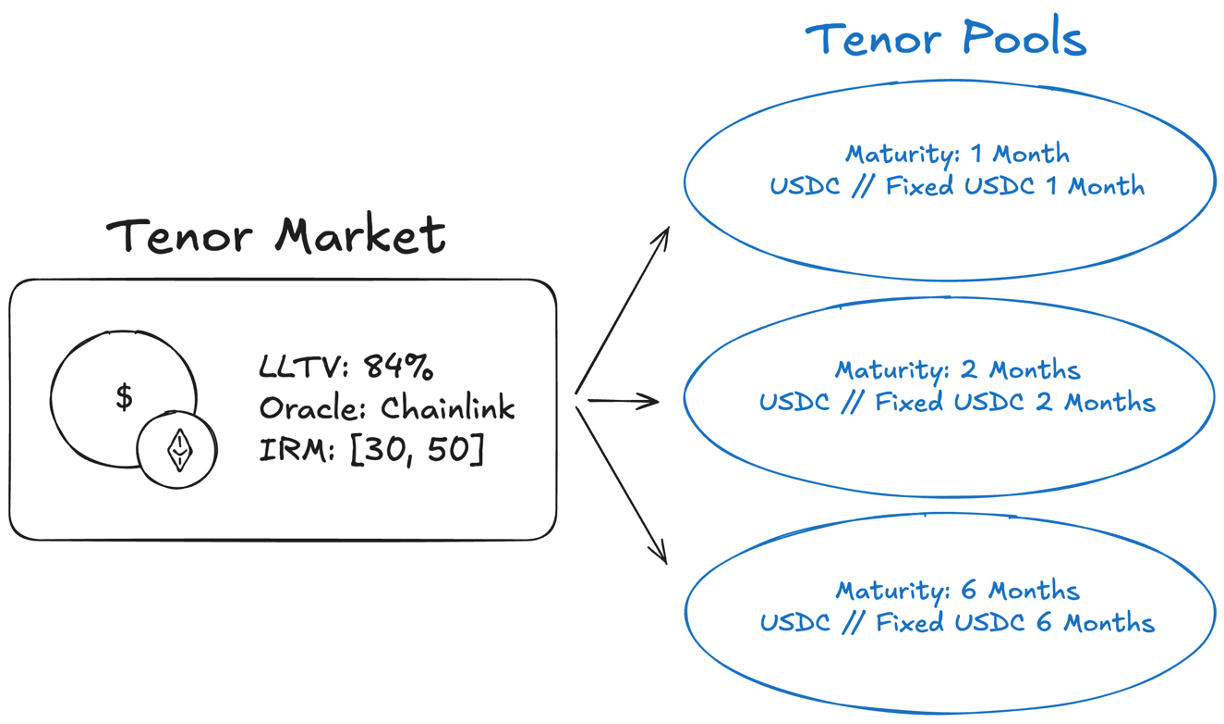

A Tenor Pool is the component of the protocol that enables the swapping of loan assets (e.g., USDC) between lenders and borrowers at a fixed interest rate for a specific maturity. As presented below, each pool is associated to one Tenor Market and has a unique maturity date. Tenor Markets can have multiple pools of different maturities.

A Tenor Market with multiple pools of different maturities leads to the creation of a term structure/yield curve on top of the underlying Morpho variable rate market.

Interest Rate AMM

Swapping of Fixed Tokens and Loan Tokens in a Tenor Pool is done using an Interest Rate Automated Market Maker (IR AMM). When a user swaps, the IR AMM finds the nearest tick (liquidity or limit) with a positive balance of the desired token.

Pool Tokens

Tenor Pools contain two types of tokens:

After swapping, borrowers receive Loan Tokens allowing them to redeem the loan asset and lenders receive Fixed Tokens allowing them at maturity to receive the tokens they lent plus the interest rate accrued.

At Maturity

When a pool matures, a borrower must deposit the amount of loan assets equivalent to his Fixed Debt Token balance. The lender receives these loan assets which correspond to the number of Fixed Tokens they owned which is equivalent to the amount of loan assets they lent plus the interest rate they accrued.

Pool Parameters

Deploying a pool for a Tenor Market only requires one input:

- The maturity date (up to 500 days)

Learn how to create a Tenor Pool in the Market Curation section.